Avoid Borrowing Blunders This Holiday Season

Fast Links

Christmas came early this year.

Ready or not, the holiday shopping season is here -- and has been for a while.

Retailers could be found rolling out Black Friday deals long before Thanksgiving week, and according to a report by McKinsey & Co., 45% of surveyed U.S. shoppers had begun their holiday shopping by early October.

To some, an earlier Black Friday may have seemed like an invitation to spend more money or accrue more debt; however, shoppers may have also used the early access to holiday cheer as a means to maintain control over their bank account and shop more mindfully this holiday season.

Putting money away -- and also planning out holiday expenses in advance -- are effective tactics to help mitigate overspending, according to Paul Golden, spokesperson for the National Endowment for Financial Education.

“The holiday spending season shouldn’t come as a budgeting surprise,” Golden says. However, he adds, all the bells and whistles that come along with the holidays, from gifts to wrapping paper, decorations, holiday parties, and more, can lead to the “potential for overspending and strain on your budget.”

Fortunately, implementing tactics like shopping lists and spending limits can help to manage cash flow and prevent overwhelming holiday debt. With that in mind, let’s take a look at how:

- U.S. shoppers plan to save, spend, borrow, and budget this holiday season

- Your own plans compare

- To prevent borrowing blunders as the holidays rev up.

While some borrowing may be unavoidable during tough times, it’s important to keep it under control. Here’s our guide to holiday spending and how you can keep your seasonal borrowing in check.

Holiday savings: How do you measure up?

According to OppU’s recent commissioned survey of American consumers, which was conducted online by The Harris Poll in October 2021, 72% had already started saving for upcoming holiday expenses.

By mid-October 2021, a number of consumers had made solid progress on their holiday savings. Forty percent of consumers had saved $500 or more, the OppU findings showed, which is the amount more than half (52%) plan to spend overall on the holiday season this year (e.g., gifts, travel expenses, etc.).

On the flip side, of those who hadn’t yet started putting money away for the holiday season, only 18% said they had plans to save in advance.

Consumers aged 35 and older who hadn’t started saving were less likely to commit to saving money for the holiday season compared to 18- to 34-year-olds. For example, of those who had not started saving by mid-October:

- 41% of 18- to 34-years-olds planned to save.

- 23% of 35- to 54-year-olds planned to save.

- 11% of 55- to-64-year-olds planned to save.

- 6% of adults 65 and over planned to save.

Do you fall into any of these groups?

Situation: You haven’t started saving for the holidays

You may not be able to put much money away if you’re just now beginning to save for the upcoming holiday season, says Matt J. Goren, Ph.D., CFP, who is the program director of the CFP Certification Education Program and an assistant professor of financial planning at The American College of Financial Services; however, you may still be able to free up some funds if you get creative.

“For most people, it might [be] too late,” Goren says. “But [if] you cut back on other expenses, there still can be some time for that. It means making sacrifices somewhere else and rearranging priorities.”

The takeaway: Plan now for next year

Even if after reducing your restaurant, grocery, or other expenditures, you find you can’t splurge too much on your holiday spending this year, there’s always time to change your financial habits for the future -- for instance, by saving a bit of money each month year-round that is dedicated to the holiday season.

Goren recommends starting to save early for next year -- ideally in January -- and potentially setting up a separate saving account that receives automated payments from your checking account. Keeping your holiday funds in a separate account can be a more effective way of saving money for later use on holiday purchases than just placing extra money in a pre-existing account that you regularly access, he says.

Goren says the following:

“If it’s literally in a separate account, where you have to log in to schedule a transfer and watch the money coming out and the balance in the gift account go down, you are concretely seeing, ‘That was going to be the thing for my daughter; that was going to be the thing I bought my mom -- but now it’s not because I’m going to spend it on this other thing.’ That really helps control spending.”

Holiday spending: How will you measure up?

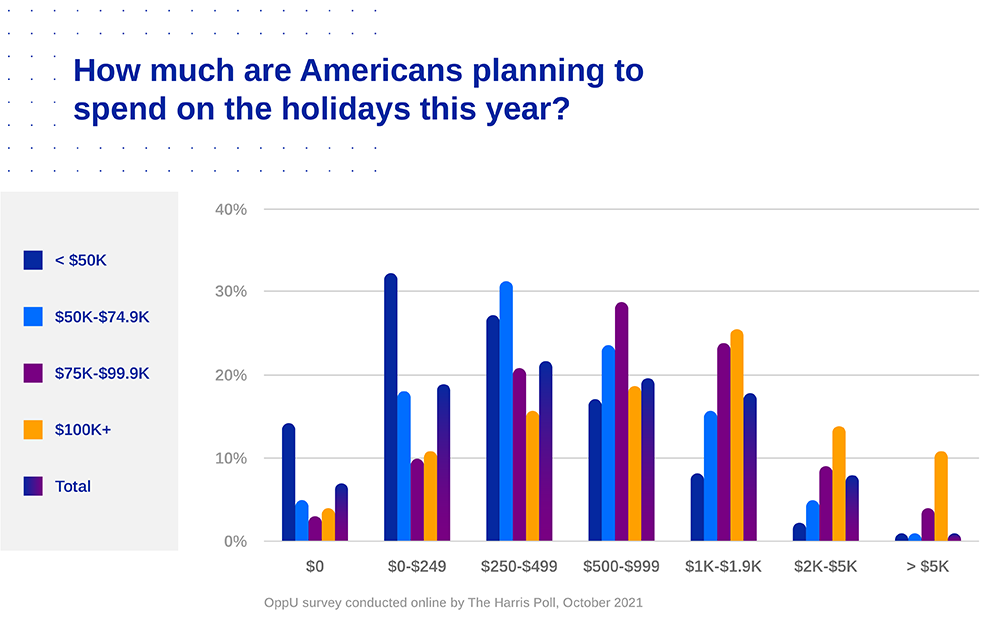

If we take a broad look at how much Americans are planning to spend on the holidays this year, some of OppU data indicates that many holiday spenders don't seem to be tightening their belts this year:

- 41% plan to spend the same amount during the holidays as last year.

- 30% anticipate they’ll spend more money.

How much are spenders planning to shell out this holiday season?

- 56% plan to spend $500+.

- 3 in 10 plan to spend more than last year.

- 19% plan to spend less than last year.

- 49% plan to spend differently than last year.

Despite the hardships many have faced due to the economic impact of the ongoing pandemic, some Americans may have had more cash on hand during the past year due to the three economic stimulus payments the federal government sent to qualifying families in 2020 and 2021.

A number of consumers, particularly middle- and high-income consumers, likely saved or used the payments to pay down debt, according to Reilly S. White, Ph.D., associate professor of finance at the University of New Mexico. However, lower-income consumers -- including workers in sectors that experienced significant layoffs, such as hospitality and leisure -- might have less spending flexibility this holiday season.

White, who is mentioned above, says the following:

“In these low-income households, you're still seeing greater uncertainty about the job market, the economy, and just less cash to go around. We’re looking at a situation where people would be dipping into their savings to fund their holiday expenses.”

Situation: You don’t have the money this year

If your budget is tight this year, you aren’t alone. According to our survey findings, a slight majority of Americans (58%) with a household income under $50,000 said they were going to spend less than $500 this season. Among these consumers, only 28% had saved up to $249, and just 14% had set aside between $250-$499.

Although 62% of consumers with a household income under $50,000 said they had started to set aside money in advance for the holidays this year, December was just over six weeks away when the survey was conducted -- and more than one-third (38%) hadn’t saved anything.

The takeaway: Set some parameters

Aligning family and friends’ expectations for gift exchanges ahead of time can help prevent feelings of inadequacy -- particularly if you feel like you didn’t get enough presents for loved ones who bought more for you. Goren suggests negotiating the rules to align with everyone’s needs:

“Maybe Christmas Eve, each person gives one gift to everyone else in a round-robin; Christmas morning, you do the same thing, and Santa also [gives the children] one present. Then you’re just filling in the boxes -- OK, we need three gifts. It’s way harder to overspend because there’s a limit.”

Alternately, family members could agree to focus on a cost, instead of quantity, says Alex Melkumian, financial psychologist and founder of the Financial Psychology Center in Los Angeles. He suggests:

“You can have a family meeting to set the rules around gift-giving, and say, ‘Hey guys, we're not going to buy anything over $100’ — or whatever amount you want to set.”

Holiday payments: How do you measure up?

Somewhat surprisingly, cash is consumers’ top payment method choice this year, with 46% saying they plan to use it for holiday purchases -- followed by money from their checking account (43%). Forty percent of consumers said they’d be paying for holiday expenses with a credit card.

Situation: You’re already in debt

Some consumers may have extra purchasing power because they've received a holiday bonus; however, not all employers hand them out -- which may mean a number of consumers rely on credit instead.

“We have millions of people who begin every single year in the hole, and then they have to climb out,” Goren says. “That's really difficult to escape; you're being dragged backward by the debt.”

Consumers can end up spending even more than they’d planned on holiday purchases due to interest rate charges and fees if they can’t afford to pay their next credit card statement in full. Some may even end up drawing from their savings to pay for the credit card debt they incurred to buy holiday items.

The takeaway: Borrow responsibly

If you’re concerned that ringing in the holidays this year may lead to lingering financial issues, there are ways to keep your borrowing in check, such as creating -- and more importantly, sticking to -- a holiday budget and not straying from your gift list.

The following tips can help you successfully celebrate without going overboard on credit card use or other forms of holiday borrowing.

Borrowing blunders to avoid

Here are 5 blunders to avoid when shopping for gifts this holiday season, especially if you plan to borrow money to pay for them.

No. 1: Overdoing in-store credit cards

It can be tempting to open a new store or rewards credit card account to land the best last-minute deals on holiday gifts, but is that really helping your situation?

While store credit cards can provide benefits such as discounts and cash back, you may want to carefully consider any sudden urges to apply for one during the checkout process.

A hard credit inquiry, which can ding your credit score, is often required to receive a retail card. As long as you make on-time payments and maintain a low balance, your score can recover. However, applying for multiple cards at once can have a longer-lasting impact.

Additionally, a number of store credit cards have a higher APR than other types of cards, which can lead to high-interest payments and spending more during the holidays than you can ultimately afford.

No. 2: Going off-book

To bypass the lure of seemingly huge sales and new product pushes, Golden suggests making a list of things you want to purchase for the holidays, and, like Santa, checking it twice — or more frequently — to see if it needs adjustments. Consider the following:

- Set a dollar amount to spend on each person.

- Once you purchase a gift for someone, cross them off your list.

- Take all of your holiday expenses into account: holiday travel, parties and potlucks, decorations, etc.

- Do not exceed your preset limits for each budget item.

- Cut your list, if necessary.

Melkumian also advises exercising discipline when you’re tempted to make holiday-related impulse buys.

“If we buy gifts for five different people, then a lot of times, we buy five different gifts for ourselves,” he says. “We then end up spending double.”

No 3: Spending money you don’t have

Cash -- which our study with The Harris Poll found is the most popular way of funding 2021 holiday season expenses -- may be a better option when you’re stocking up on holiday goods. An empty wallet can serve as a visual cue that the allotted amount you planned to spend is gone, and it’s time to stop shopping.

Also, remember to shop smart. Inflation, supply-and-demand, and other economic factors may result in sticker shock when consumers start their holiday shopping, according to Goren -- who says even when those elements aren’t an issue, people typically tend to overspend.

“That's true even more this year when inflation's been higher than it has been in decades, so everything is surprisingly expensive. We might really see some price gouging -- because unlike buying a couch, where you can wait, there are these hard deadlines. Christmas is always on the 25th of December.”

Allowing enough time to hunt down the best price for holiday items -- and doing some comparison shopping -- can help you avoid overspending. Be careful, though, White says, not to jump on a purchase just because you’re thrilled to find it’s in stock. He says:

“If things aren't available because of supply chain issues, or it’s twice the price online versus what it should be, I advise always wait, wait, wait until the supply chain issues are shorted for expensive items,” he says. “Don't spend more than you should.”

No. 4: Buying gifts people don’t need

Our survey found 49% of the consumers who plan to spend money during the holidays say their spending will be different this year compared to last year, while 30% will spend more.

Trying to make up for lost time this holiday season can be a prime scenario for spending too much -- which is why Melkumian says it’s key to keep your feelings in check when shopping.

“When we're dealing with something as unique as a pandemic, we're much more likely to be more emotional,” he says. “Then that emotion is clouding our judgment --‘Even though I can't afford it, I will go against all conventional wisdom just to convey my love for the family I haven't seen.’ Financial health is really about planning and staying within certain boundaries and limits.”

If, for instance, your budget won’t allow for show-stopping gift-giving this year, focusing on more experiential options may be a way to express your care without incurring excessive debt.

“The idea is it's not about the money, but enjoying ourselves and our family and having experiences together,” Melkumian says. “Five or 10 years from now, you're not going to remember that purse; but you're going to remember, ‘Hey, we actually did this really cool thing with mom and dad.’”

No. 5: Borrowing from yourself

Spending too much during the holiday season can cause additional stress if you’ve been struggling financially.

If you’re truly struggling to save for retirement or would need to tap into an emergency fund to pay for an outing or other gift, you may want to consider an alternative approach.

"What are the things you need to spend money on -- housing, transportation?” Goren says. “Are you prioritizing the future and thinking long-term? Until you've got your finances figured out, gift your time; your talents -- things that don't cost money and are probably going to be more appreciated by the people you're gifting them to."

The bottom line

Overspending during the holiday season can be easy to do, especially if you don’t have the right measures in place to protect your bank account. Fortunately, implementing tactics like using detailed shopping lists and purchasing limits can help manage your cash flow and keep your spending habits in line, especially in a season that can be ripe with holiday sales.

Methodology

This survey was conducted online within the United States by The Harris Poll on behalf of OppU from October 14 - 18, 2021 among 2,042 adults ages 18 and older. This online survey is not based on a probability sample and therefore no estimate of theoretical sampling error can be calculated. For complete survey methodology, including weighting variables and subgroup sample sizes, please contact oppu@opploans.com.